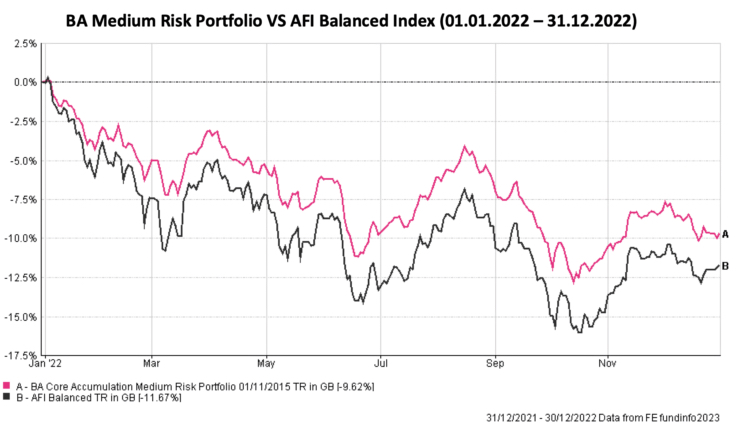

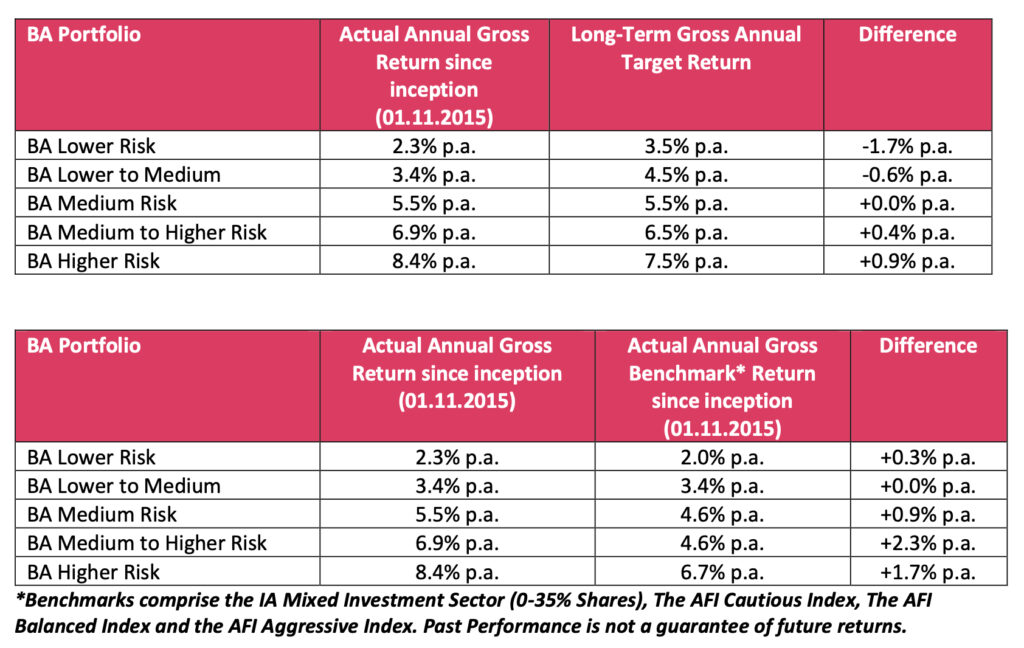

As mentioned in our previous updates, when markets are volatile, ensuring your portfolio is highly diversified provides an effective level of protection against that volatility. With this in mind, whilst 2022 has been a very challenging investment environment, our investment approach of providing a diverse, risk rated and lower cost solution has held up well over 2022 on a comparative basis. This can be demonstrated in the following chart which compares our medium risk investment portfolio to the industry benchmark over the past 12 months.