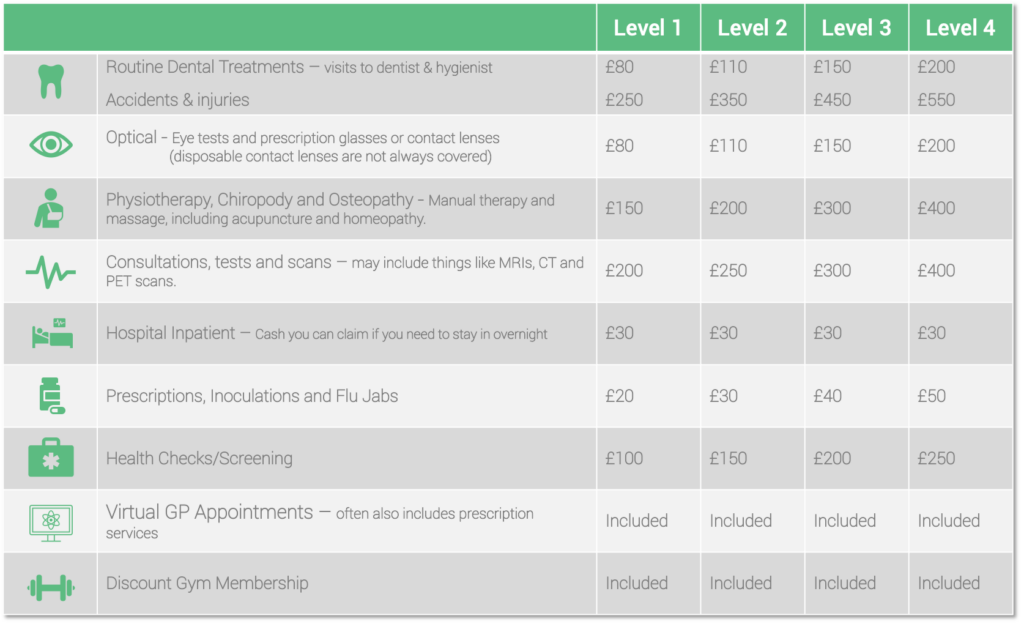

| Core Purpose | Reimbursement for everyday healthcare costs (routine care) | Covers diagnosis and treatment of acute medical conditions (serious/new illness or injury) |

| Typical Coverage | Dental, optical, physiotherapy, osteopathy, prescriptions | Private consultations, diagnostic scans (MRI/CT), hospital treatment, surgery |

| How it Works | Pay upfront and claim money back up to annual limits | Insurer pays provider directly (subject to policy terms/excess) |

| Average Cost | £10–£30 per month | £40–£120+ per month (can be much higher depending on cover) |

| Employer Uptake | Approx, 2–2.5 million employees | 4.7–4.8 million employees covered via employer schemes |

| Market Position | Smaller but fast-growing “everyday health support” benefit | Larger, established private healthcare access benefit |

| What it Does NOT Cover | Major surgery, hospital treatment, serious conditions | Routine dental/optical care, most everyday health expenses |

| Typical Use Case

| “Help me manage routine healthcare costs” | “Get me fast access to diagnosis and treatment” |

| Employer Value Proposition | Low-cost wellbeing perk, reduces out-of-pocket spend | High-value benefit to reduce waiting times and improve access

|

Money Mindset: The Financial Impact of Grief

Previous post

Money Mindset: The Financial Impact of Grief

Previous post